ULIP Investment Agentic AI Solution for Customers

Already 34% of Indians had a term insurance by the end of 2025 and they collectively paid 8.85 lakh crore rupees a year on insurance premiums, according to DD News. The number of people with term insurance has been growing at the compound annual growth rate (CAGR) of about 13 per cent over the last 20 years. For insurers in India, that number will translate into crores of new customers (i.e the end customer of the insurer) in the coming years if they can overcome a bottleneck.

From a customer's perspective, purchasing term insurance or a ULIP in India hasn't changed much in the past 20 years. It typically starts with an agent who is often a relative, neighbour or someone from the local branches calling to discuss "investment-cum-protection" options. The agent visits in person, sometimes more than once and collects handwritten or photocopied KYC documents (Aadhaar, PAN, address proof). Along the way, the customer is frequently nudged toward a ULIP over pure term cover, with promises of returns, bonuses and maturity benefits.

The process involves filling out lengthy paper proposal forms, declarations about medical history and nominee details. The agent submits these to the insurer and the customer enters a waiting period coordinating with the agent for updates, unsure whether the policy is approved, pending medical tests or stuck in underwriting. For higher sum assured amounts, a medical examination is scheduled separately, adding more days. Bank mandates for premium payments are set up manually via NACH forms.

Between the first conversation and the policy document landing in the customer's inbox or more often, arriving as a physical booklet by post, it takes anywhere from a week to three weeks.

Against this backdrop, any insurer in India that can deliver a policy document to the customer within minutes, fully compliant with IRDAI regulations, stands to gain lakhs of new customers and crores in additional premium income. The competitive advantage is significant : in a market where customers are increasingly comparing options online and dropping off during long wait times, speed and transparency are differentiators. Recent advances in Agentic AI make this not just possible, but practical to deploy at scale.

Overview of our Voice-Based Agentic AI Solution

Filling out a long application form, suggesting insurance plans based on customer’s preferences, and collecting KYC details are the tedious activities in the insurance industry. It is also where the Agentic AI Solution for ULIP Origination delivers the fastest return on investment. It has been designed for Indian insurers and Indian customers and here are some of the benefits it offers to the companies and to the customers.

Advantages for Companies

The AI Agent can

-

Seamlessly guide a customer through multistep insurance forms providing them an enhanced customer experience. It has been tested to help customers fill large term insurance applications with >75 unique fields.

-

Integrate with the email service that the insurer uses. After integration the AI Agent can send policy documents to the customer for their review, update the policy documents after the changes suggested by the customer, and share secure payment links. Integration with communication channels such as WhatsApp is also feasible

-

Verify the mobile number, PAN number, Aadhar details of the customer using OTP verification service and core system APIs

-

Integrate with CRMs such as Zendesk, Freshdesk, Salesforce etc where the customer information obtained during the application process is seamlessly updated in a single ticket and handed over to the insurer. This makes the agentic AI Agent auditable and also provides necessary human oversight.

Note : Capturing every interaction in a CRM also gives the insurer full visibility into applications where customers have dropped off mid-journey, whether at the KYC stage, during medical declarations or at payment. Rather than losing that business silently, the company can trigger timely follow-ups through the agent or directly to the customer, recovering leads that would otherwise go cold. In a market where acquisition costs are high, plugging these drop-off points can meaningfully improve conversion rates and protect premium income.

Advantages for Customers

A lot of the technological development in the insurance industry in the past couple of decades has been behind the scenes. Although there have been great improvements in customer experience, the process of applying for insurance in a brick-and-mortar office hasn't changed much. In many places a customer still has to submit physical copies of their documents. The ULIP Investment Agentic AI Agent provides a thorough overhaul of the entire insurance application process.

-

Apply over call: The customers can apply for a term insurance, learn about all the applicable offers, submit documents and get their insurance policy documents all over the span of a call. There are no forms to fill out independently, no confusion midway through an application, and no need to call back a contact centre because something was unclear or filled in incorrectly

-

Support for Indian languages: In a country where only 6% of the population speaks English as per Oxford, the AI Agent converses with customers in their own vernacular languages, ensuring that language is never a barrier to getting insured. Multiple Indian languages are supported, with more available on demand from the insurer

-

Real-time guidance throughout: Rather than leaving customers to navigate complex coverage options alone often resulting in wrong choices or under-insurance the AI Agent actively guides them through every decision, ensuring they understand what they are buying and why

-

Built for how India uses the internet: With the majority of Indians accessing the internet on mobile devices, desktop-first forms have long created a broken experience for most customers. The AI Agent is designed for a mobile-first, voice-first reality, eliminating the friction that causes drop-offs.

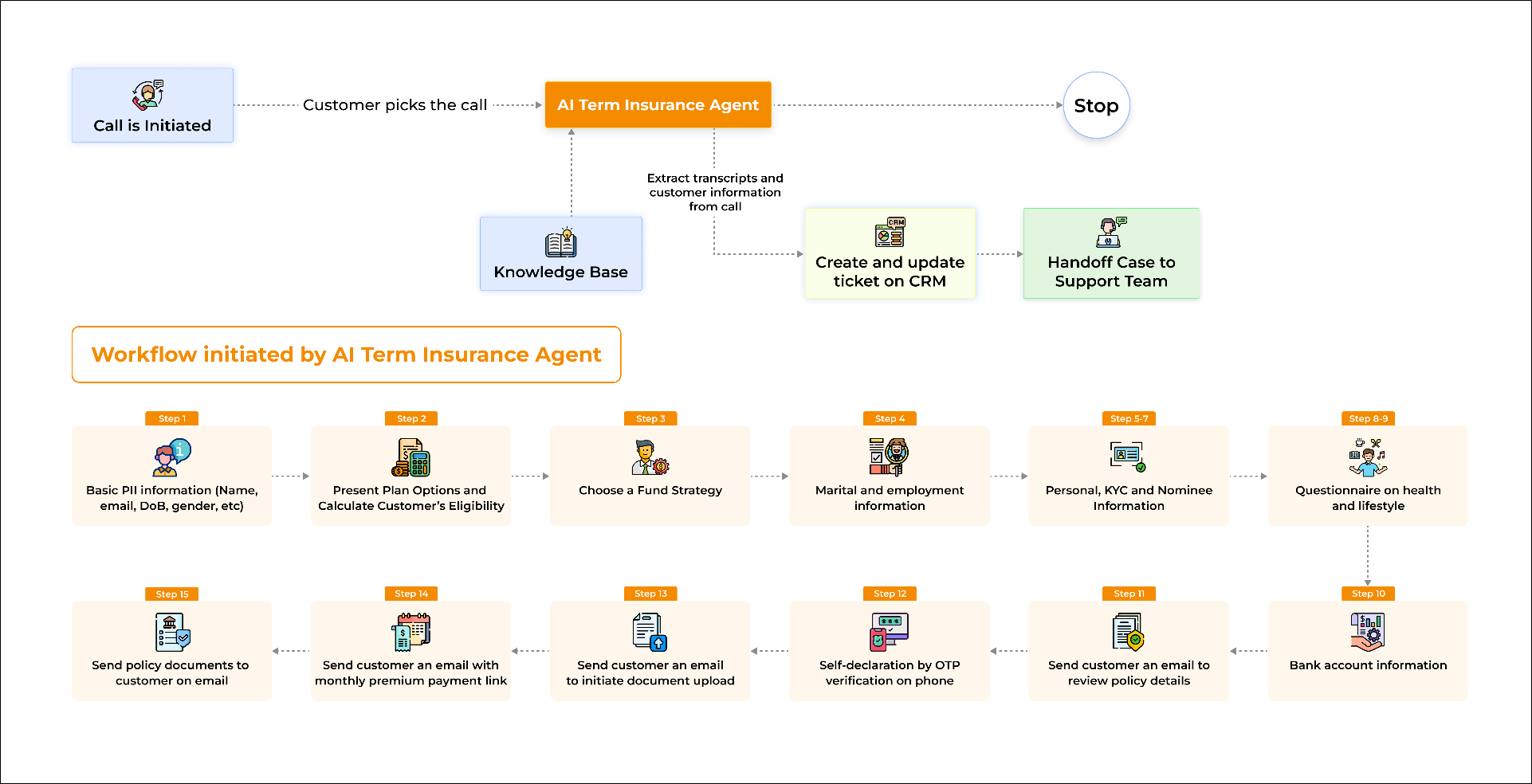

Voice-based Agentic AI Solution for ULIP Origination in Action

This section illustrates how the Voice-based Agentic AI Solution for ULIP Origination functions .

IMPORTANT : Please note that the steps shown are illustrative. All workflow steps are fully customizable and tailored to each insurer's products, rules and processes.

In this section, the voice-based conversation between a customer and an Indian insurer is used to show the AI Agent’s workflow. We have configured 15 steps in this AI Agent and each step has a set of questions and validations.

Please note that all the fields, their ordering and their corresponding values are completely configurable in nature.

In this example, we have set up an “AI Term Insurance Agent” which will guide the customer through the entire application and eventually hand over the case to the insurer as a ticket on the CRM. The AI Term Insurance Agent can also be trained on the insurer’s knowledge base, enabling it to answer product questions, explain coverage options and provide real-time guidance, without ever leaving the conversation.

Following steps are followed by the AI Agent:

Step 1: Collects Basic PII Information

The AI Agent collects customer basic PII details, including the customer's name, gender, mobile number, date of birth, email ID, and annual income range.

Step 2: Shows Plan Options & Calculates Eligibility

The customer is shown several plan options and the AI Agent calculates the customer's eligibility for the insurance policies selected by the customer. Customised calculation tools guarantee optimum accuracy in calculations. In this process, the factors that decide eligibility for a given plan include:

Step 3: Displays Fund Strategies

The customer selects a fund strategy which suits their needs. Options given are aggressive, moderate and conservative.

Step 4: Gathers Marital and Employment Information

The AI Agent collects marital and employment information about the customer. It asks about the customer’s marital status, education, occupation, pincode, nationality, and other details.

After sharing all the details, the customer is asked to give their explicit consent for searching CKYC records from the Central Records Registry. The AI Agent will not proceed further with the application if the PAN details don't match with the CKYC records.

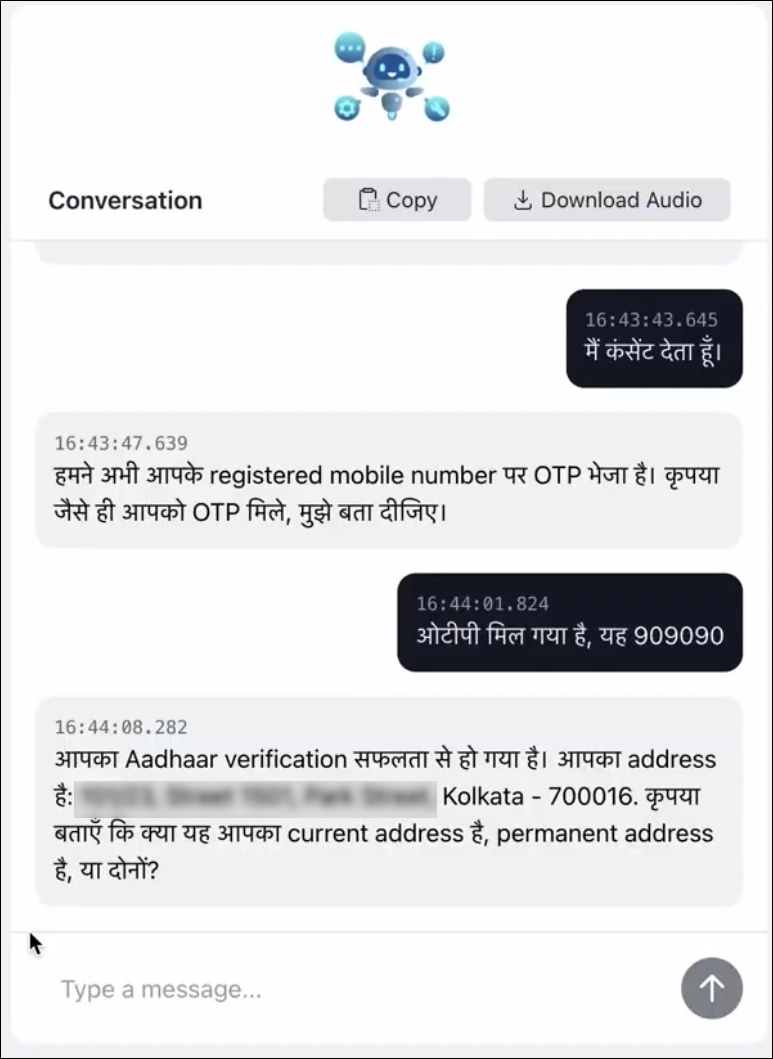

Step 5: Gets KYC information

The Aadhar details, such as the customer's date of birth, current address, and permanent address, are verified in this section. The customer is asked to give their consent for Aadhaar verification, confirm that they agree to receive all policy-related documents and communications electronically on the email address provided in the proposal form, and indicate whether they would also like a physical copy of the policy document in addition to the electronic one, following which an OTP is sent to complete the verification.

Fig. A transcript demonstrating mobile OTP-based verification for Aadhaar authentication

Step 6: Obtains Compliance Information

The AI Agent collects the customer's compliance and tax-related information through a brief set of yes/no questions such as covering any history of criminal conviction in India or abroad, whether they are a Politically Exposed Person or a close relative of one, whether they are a tax resident of any country other than India and whether they hold an Electronic Insurance Account (EIA).

Step 7: Learns About the Nominee

In this step, the AI Agent collects information about the nominee. The customer is prompted to tell the nominee’s name, date of birth, communication address and the customer’s relationship with the nominee.

Step 8: Gathers information about customer’s health details

Now the customer is asked to share their health details. The customer is asked to share their height and weight and answer questions about cigarette, tobacco, and narcotics consumption.

Step 9: Gathers detailed information about customer’s health history

In this step, the customer is asked more questions about their health. The questions are about diseases–such as cholesterol and diabetes–hospitalization history, mental disorders and questions about the health of family members.

Step 10: Collects Customer’s Bank Account Details

In this step, the AI agent asks the customer to securely share their bank account details. The monthly insurance premium is deducted from the shared bank account. The customer has to provide their bank account number, name of the account holder, IFSC code and account type.

Step 11: Sends an email to customer to confirm policy details

The AI agent sends an email to the customer to confirm and verify the details collected for the policy. If the customer wishes to modify any details at this stage, they can request the AI agent to make the necessary changes. Once updated, a revised email with the corrected details is sent again. If no further changes are required, the customer is then asked to provide their consent.

Step 12: Assists customer with self-declaration

The customer is guided through the self-declaration process by answering the required questions, after which they complete e-verification of their application via OTP. The OTP is sent to the customer’s mobile number

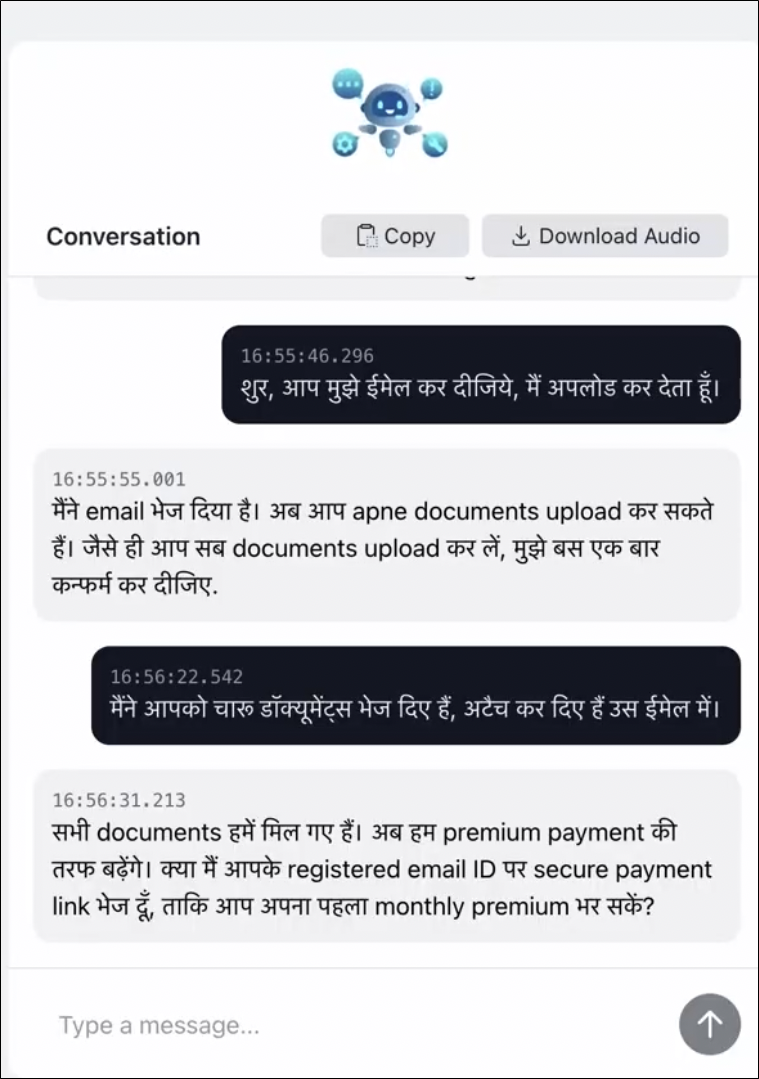

Step 13: Assists customer upload necessary documents

In this step, the customer is asked to share the electronic copies of their identity proof, address proof, income proof and age proof through an email.

Fig. A transcript of a conversation where the AI Agent is guiding customer to upload necessary documents over an email

Step 14: Sends email to customer to initiate their First Premium Payment

A secure payment link is shared with the customer via email, allowing them to conveniently complete their first month’s premium payment.

Step 15: Shares Policy Documents on email

The policy documents are securely shared with the customer via their registered email address for their reference and records.

AI Agent and Real World Scenarios

The sample flow outlined above represents an ideal scenario. However, the Voice-based Agentic AI solution for ULIP origination is designed for real-world conditions and is equipped to handle real-world scenarios.

Scenario 1 : Customer drops-off during the flow

During their interaction with the AI agent, a customer may choose not to complete the journey for various reasons. The most common scenarios include :

-

The customer does not consent to the insurance terms

-

The customer is not ready to make a premium payment immediately

-

The customer is unable to complete the application due to time constraints or a change in intent

In such cases, the AI agent proactively asks the customer for a convenient time to reconnect. Once the customer provides a preferred time (for example, 2 p.m. three days later), the AI agent automatically creates a ticket in Zendesk, enabling a human agent to follow up with the customer at the scheduled time.

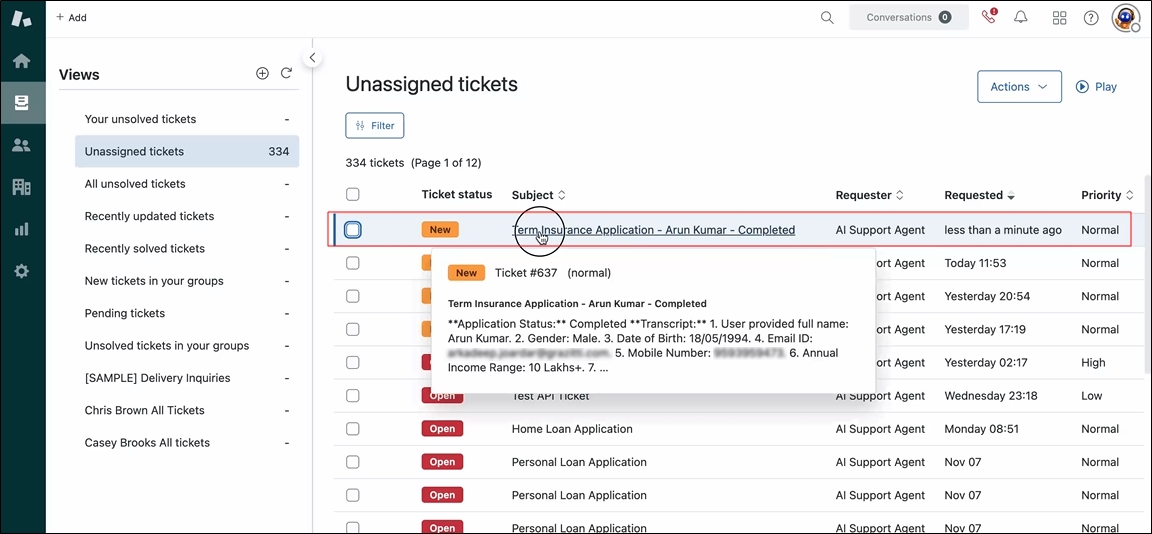

Scenario 2 : Customer Call Gets Disconnected

In the event of a call disconnection, the AI agent automatically creates a ticket/ case in a CRM (e.g Zendesk, Salesforce, Freshdesk, etc.), capturing the call transcript along with all relevant details gathered up to that point. The ticket is then assigned for a human agent to review and take appropriate follow-up action.

Fig. A snapshot of a ticket created in Zendesk (CRM) by the AI Agent.

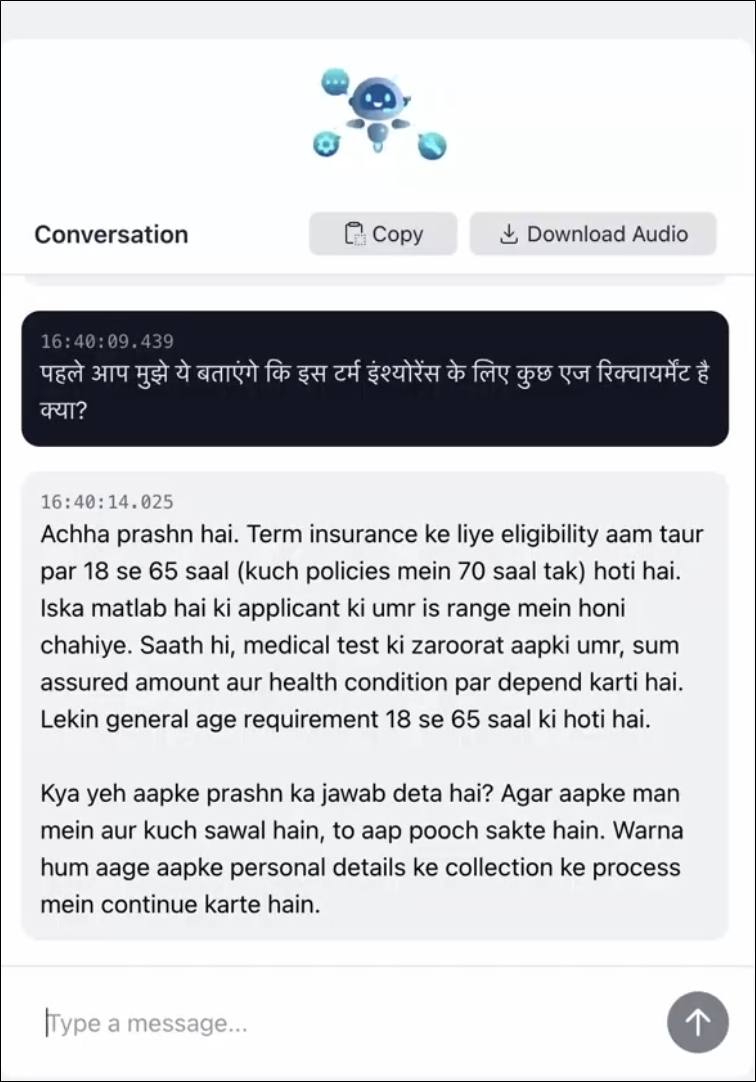

Scenario 3: Customer Asks an Off-flow Question

During the conversation, the customer may ask questions related to the policy they are considering or even unrelated queries. The AI agent is capable of addressing such questions from the knowledge base and then seamlessly guiding the conversation back to the policy purchase journey.

If the required information cannot be retrieved with sufficient confidence from the knowledge base, the AI agent, guided by predefined guardrails, responds gracefully, informing the customer that the query is beyond its current scope.

Fig. A transcript of an off-flow question asked during the policy purchase journey